You don’t price the wrong clients. But you may be pricing the wrong thing.

MTD of Income Tax did not add four submissions. Change that you are responsible for.

In rooms full of refugees and accountants, anxiety isn’t software. It’s a conversation.

“How do I charge for this without losing customers?”

Here’s what we’ll cover:

IE-Book: Income Tax MTD—The ultimate step-down book of procedures

Accountants and bookkeepers still have time to develop an iterative plan for MTD success. This e-Book explains how, with an agile mindset, and a 5-step countdown to April 2026—and beyond.

Get Tax Digitization: The Final Countdown Playbook

The legend of MTD

“It just pushes a button.”

Quarterly updates. A suggestion. Clicking.

From the outside, that’s all MTD looks like.

Therefore, the price increase is felt to be small.

But what’s changed isn’t the button—it’s everything behind it.

The visibility gap

Clients see the post. You bear the responsibility.

Clients see:

- Deadline

- Number

- Guarantee

What you really have:

- Chasing missing records

- Cleaning up incomplete data

- Reviewing consistent classification

- Continuous debt

The client sees the post. You are dangerous if it is not right.

Your pricing problem lies in that gap.

| What clients see | What you have |

| Posted | The chase |

| Buttons | Clean up |

| Deadlines | Review the risks |

| Admin | A continuing obligation |

“It takes too long to do a consolidation presentation, because you have to cross all the boxes.”

Rebecca Benneyworth,

Tax consultant and MTD Working Group member, ICAEW MTD Live

Moral background

The real cost driver is not shipping. Behavior.

Under the Income Tax MTD, the cost depends on:

- How clean are the records

- How fast information comes

- How often maintenance is required

- How involved is the client

Two clients. Same benefit. Four similar reviews.

- A person sends a structured spreadsheet.

- Someone posts 47 untagged transactions and a picture of a shoebox.

Same income. Four jobs.

Same money?

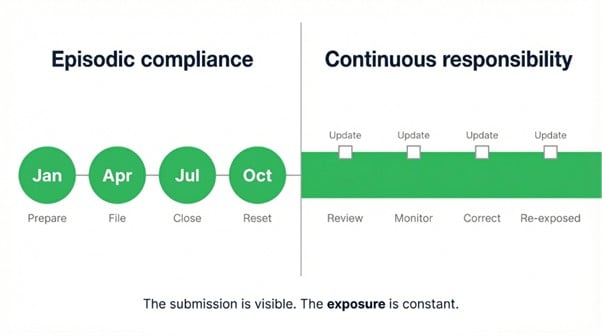

Change of responsibility

The task no longer has a finish line.

Prior to MTD, work sounded like an episode:

Configure → File → Close → Reset.

Under MTD of Income Tax:

- Records are rarely completed

- Oversight continues

- Risk does not disappear in transit

- Mid-year delivery is messy

The bond is not reset. It rolls forward.

You cannot opt out of MTD shift. Only you can decide if the price is worth it.

That is a structural change.

“That filing is a responsibility. It’s a deadline we have to work to. If the clients don’t deliver, that changes everything.”

Rebecca Benneyworth,

Tax consultant and MTD Working Group member, ICAEW MTD Live

Model under shift

This is a A Continuous Commitment Model: structural change from episodic to continuous exposure shaped by client behavior.

It is not a price adjustment. A separate economic unit.

And the economic unit in which you set prices is no longer a proposition. Exposure.

IE-Book: Income Tax MTD—The ultimate step-down book of procedures

Accountants and bookkeepers still have time to develop an iterative plan for MTD success. This e-Book explains how, with an agile mindset, and a 5-step countdown to April 2026—and beyond.

Get Tax Digitization: The Final Countdown Playbook

Why prices break

If you only call the visible layer (“four updates”, “just a button”, “raise the boss”), you miss:

- Behavioral diversity

- Continuous review

- A constant risk

And thus the margin leaks—one invisible hour at a time.

If volume is already strong, those invisible hours can reduce profits. And even squeeze new work.

The decision

When you move prices, you bet on the perfect behavior of clients.

When you pay the price, you pay the real price.

You can sell MTD as:

Or you can call it:

- An ongoing obligation shaped by the behavior of the client

Only one protects your margin when behavior changes.

What does this mean in practice

MTD won’t break your rates because you charge less.

It will break because the economic model has changed.

If the bond continues, then the values should be the same

For example:

- Category prices based on quality behavior

- They are stored every month rather than year round

- Obvious obligation clauses in engagement letters

- Price updates linked to behavior

Hannah Miller, managing director of Chipperfield Accounting, explained that it requires clients to submit data within 14 days of the end of the quarter as a condition of monthly payments—making the payment structure a dual commitment rather than a single charge.

ICAEW MTD Live

This is not a theory. Practices are already priced using the Continuous Responsibility Model—it just doesn’t have a name yet.

Diagnostic questions, client negotiation frameworks, and pricing frameworks that reflect ongoing exposure rather than volume are fully developed here.

Sign up for the Sage Advice newsletter

Join over 500,000 UK readers and get the best business management tips and tricks, as well as actionable advice to help your company succeed, delivered to your inbox every month.

Register now